Divorce can take an enormous toll on a person.

Even where both spouses know the marriage is over, the process can be emotionally draining, financially stressful and deeply unsettling. People are often trying to protect their children, preserve some dignity, avoid unnecessary conflict and keep control of costs.

So it is completely understandable that many people look for the simplest and cheapest route available.

They may not want a fight. They may not want solicitors involved. They may not want to spend money they fear they will need later. They may feel that if they can just get the paperwork done, they can move on.

In some cases, that may be fine.

But where there is a family home, a pension, a business, inheritance, savings, investments, or a real difference in earning power, divorce is rarely just paperwork.

It is a major financial event. The decisions made at that point can affect both people for many years.

That is why the cheapest option at the start can become the most expensive option in the long run.

Why people choose the cheapest route

Most people do not choose a cheap divorce because they are reckless. They choose it because they are tired.

They want peace. They want certainty. They want to move on. They may have spent years in a difficult marriage and do not want the divorce itself to become another source of conflict.

There is also a very normal fear of legal costs. People hear stories about expensive divorces and think the safest thing is to keep lawyers out of it as much as possible.

That instinct is understandable. Nobody should spend money on legal work they do not need.

The difficulty is that people often judge the cost of divorce only by the bill in front of them. They do not always see the value of what proper advice may protect.

It is a bit like choosing not to pay into a pension, not taking out insurance, or not getting tax advice before selling an asset. The saving feels real now. The cost may only become clear years later.

Why legal fees can feel so expensive

One theme that comes up again and again in personal accounts of divorce is the cost of legal fees in Ireland.

People remember the bill. They remember the stress. They remember the feeling that the process took longer than they wanted. What is often harder to see is the financial damage that may have been avoided because proper advice was taken at the right time.

Family law work also takes more time than many people realise. A divorce involving assets may involve financial disclosure, correspondence, settlement meetings, court documents, negotiations, pension issues, mortgage issues, tax questions and advice on what may or may not work in practice.

If there are no meaningful assets, that level of work may not be needed.

But where there is property, a pension, a business or a major difference in financial position, the fee should be judged against what is at stake.

A person may feel that spending €15,000 or €20,000 on a divorce is very expensive. In the right case, it is. But if the advice protects a pension, a home, a business, or a fair financial settlement, the cost has to be seen in that context.

A simple process does not make your finances simple

The danger with low-cost divorce services is that people mistake a simple process for a simple case.

A form-based divorce may help move paperwork through the system. It will not necessarily tell you whether the agreement is wise. It will not value a pension. It will not explain whether giving up your interest in the family home is sensible. It will not tell you whether a maintenance agreement will still work in five years. It will not spot every issue around a company, inheritance, tax, or future housing needs.

That is the distinction people often miss.

The paperwork may look straightforward, but the consequences can be much harder to fix.

People are entitled to represent themselves. Many do. The difficulty is that some only look for legal help after the agreement has become unworkable, the paperwork has gone wrong, or a major asset was never properly considered.

By then, the choices may be much more limited.

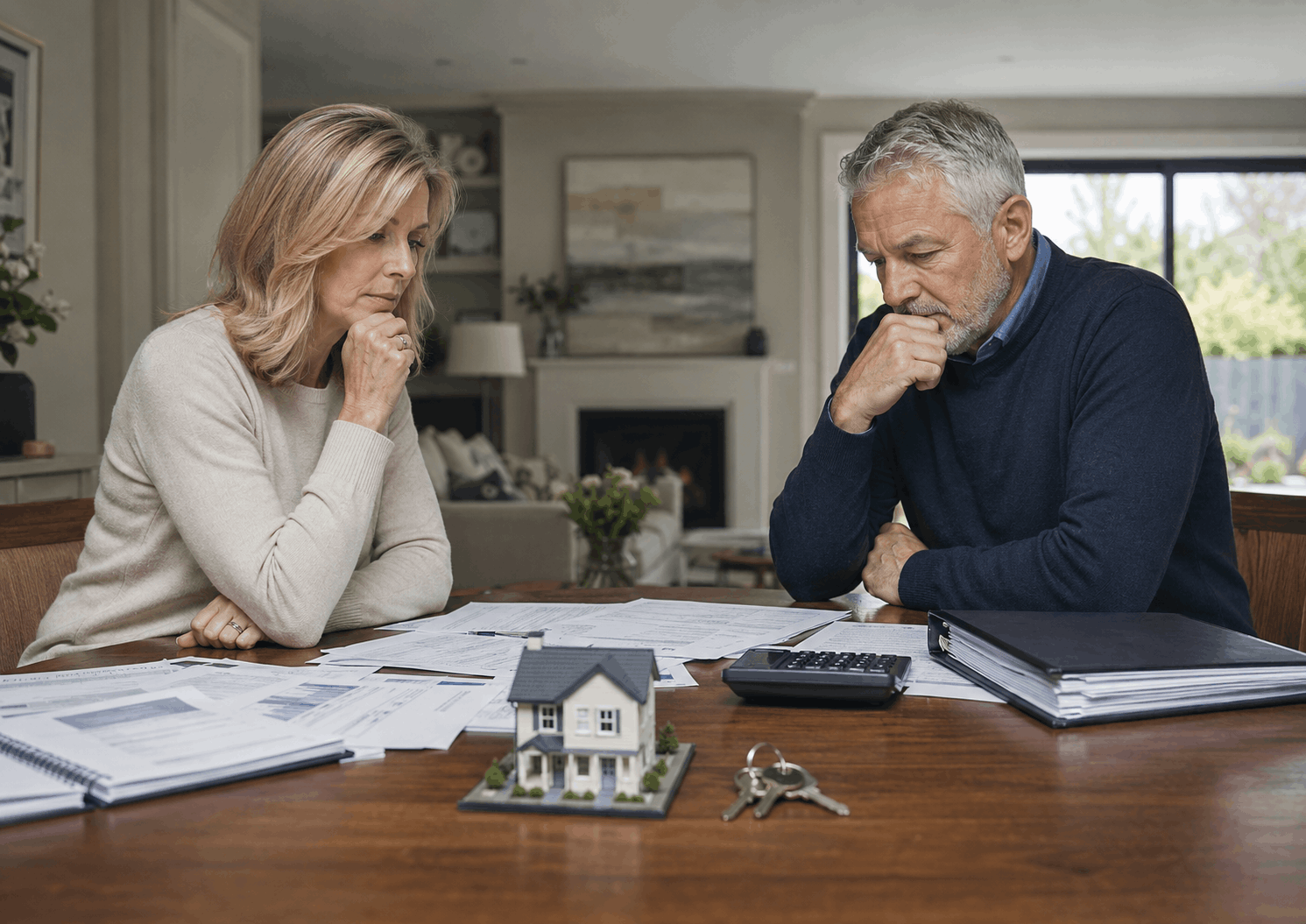

The family home is where many mistakes happen

For most couples, the family home is the largest asset.

It is also the asset people make emotional decisions about. One person may agree to leave because they do not want tension. One may agree to a sale because they want the matter over. One may accept a buyout figure because it sounds reasonable. One may keep the house without looking carefully at whether they can afford to do so.

These decisions can feel practical at the time. They may also be very costly.

If you give up too much of the home, you may not be able to buy again. If you keep the home without enough income, you may be left under pressure. If you agree a figure without advice, you may find later that the value, mortgage, tax position or trade-off with other assets was not properly understood.

The family home should not be treated as a box to tick in a divorce. It can shape both people’s financial lives long after the marriage ends.

Pensions are often ignored because they feel distant

Pensions are another common problem in cheap or rushed divorces.

People tend to focus on what they can see: the house, the bank accounts, the car, the monthly bills. A pension can feel distant. It may not feel like real money, especially if retirement is still years away.

That can be a serious mistake.

In some marriages, the pension is one of the most valuable assets. One spouse may have built up a strong pension through employment or a business. The other may have a much weaker pension because they took more responsibility at home or worked reduced hours.

If that is not looked at properly, the outcome may look fair today but become unfair later. One person may be secure in retirement. The other may not.

Take a simple example. A person may feel they have done well because they are receiving a good share of the equity in the family home. They may decide not to raise the other spouse’s pension because they do not want to rock the boat.

But if that pension could produce €30,000 a year in retirement, even a partial claim may be worth far more than the legal fees they were trying to avoid. Over 20 years, that could amount to hundreds of thousands of euro.

That may be the difference between a comfortable retirement and having to be extremely careful with money later in life.

Pensions also involve technical work. It is not enough to say, in broad terms, that a pension will be shared. The right orders may need to be made. The pension trustees may need to be involved. Death in service benefits and retirement timing may need to be considered.

This is exactly the kind of long-term issue that can be missed when the main aim is to get the divorce done quickly and cheaply.

“We have agreed on everything” may not be enough

Couples often say they have agreed on everything.

That may be true. It may also mean that one person has agreed to terms without knowing what they are worth.

A person can agree because they feel guilty. They can agree because they want to avoid conflict. They can agree because they trust the other person. They can agree because they think asking for more would make them look greedy. They can agree because they are exhausted.

None of that means the agreement is sound.

Both people signing an agreement does not automatically make it a good one. It should be based on proper financial information, a clear understanding of the assets, and a realistic view of what each person will need after the divorce.

That is especially important where one spouse has always dealt with the money, the business, the investments or the tax affairs.

Mediation is not the same as legal advice

Mediation can be very useful in the right case.

It can help people reach an agreement without turning every issue into a fight. It can reduce stress and legal costs. It can also give both people more control over the outcome.

But mediation is not a substitute for legal advice.

A mediator’s role is to help the parties reach agreement. A mediator is not there to advise one spouse that the agreement is a poor deal for them. Even where a mediator has legal training, that is still not the same as acting for either person.

This matters because people can leave mediation believing everything is sorted, while still not understanding the long-term effect of what they have agreed.

A mediated agreement should usually be checked before it is finalised, especially where there is a home, pension, business, maintenance issue or financial imbalance.

Cheap divorce can be risky for business owners

A low-cost divorce is rarely suitable where one or both spouses have a business.

Business ownership can make the financial picture much harder to read. Income may not be straightforward. Value may sit in shares, retained profits, property, loans or company assets. A person may have access to resources that do not show up as ordinary salary.

There may also be tax issues. A settlement that looks sensible on paper can have consequences that neither spouse has thought through.

This does not mean every business divorce has to become hostile. It means the business has to be understood before decisions are made.

If it is not, one person may give away too much. The other may agree to something they cannot fund. Both may end up back in dispute later.

An agreement has to work in practice

A divorce agreement can look tidy on paper and still fail in real life.

One spouse may agree to take over the mortgage without checking whether the bank will approve it. A pension may be divided in principle without the pension trustees being able to give effect to it. A business payment may be agreed without checking whether the company can fund it. The agreement may say what should happen, but say very little about what happens if one person does not do what they promised.

These are not minor details.

They can decide whether the agreement actually works.

This is one of the main reasons proper advice matters. A solicitor should not only look at what has been agreed. They should look at whether it can be carried out.

Proper advice does not mean starting a fight

One reason people avoid advice is that they fear it will make the divorce more aggressive. That is not what good advice should do.

Proper advice should help you understand what matters, what is worth arguing about, and what is not. It should help you avoid emotional decisions. It should help you settle where settlement is sensible. It should also stop you from agreeing to something that could damage your future.

In many cases, advice reduces conflict because it brings clarity. People are less likely to argue around vague fears when the assets, risks and options have been properly explained.

Good advice should not make the divorce more hostile. It should help you avoid agreeing to something you may later regret.

It can also provide a buffer.

Most people negotiate a divorce once in their life. Family law solicitors deal with these issues every week. They know where agreements tend to break down, what an Irish court is likely to ask, and which points matter more than they first appear.

That can be particularly important where one spouse is more confident, more financially informed, or more willing to push for what they want.

The court may not fix every bad agreement

Some people assume that if an agreement is unfair or incomplete, the court will simply fix it.

That is a risky assumption.

In Irish divorce, the court must consider whether proper provision has been made. But the courts in Ireland can only work with the information put before it. If assets have not been properly valued, if pension issues have not been explained, if mortgage approval has not been checked, or if the agreement does not deal with what happens when something goes wrong, the court may not have a full picture.

Judges do look at agreements. They do not simply ignore the parties’ wishes. If both spouses say they are happy with an arrangement, and the agreement appears broadly fair on the information available, it may be approved.

That can create real problems later if the agreement was built on incomplete information or unrealistic assumptions.

Can you afford to divorce?

This is a difficult question, but it is one people need to ask honestly.

Some people cannot afford to divorce in the way they first imagined. The money may not stretch to two homes. A business may not be able to fund a large payment immediately. A pension may be valuable but not accessible now. A family home may need to be sold even though neither person wants that.

These are hard realities. Ignoring them does not make the divorce cheaper. It usually makes the eventual problem worse.

A proper financial review at the start may show that a person needs to wait, negotiate differently, protect a particular asset, or accept that a preferred outcome is not realistic. That advice may be uncomfortable, but it is far better to know early than to find out after signing terms.

The real cost is not the fee

The fee may be small, but the mistake may not be.

The bigger cost may show up later, when someone realises a pension was never valued, too much of the home was given away, the maintenance arrangement was too loose, a business was never properly checked, or a tax issue was missed.

Those mistakes can cost far more than early advice would have cost. They can also be hard to undo.

By the time someone realises the agreement was poor, the other spouse may have moved on, assets may have changed, the house may have been sold, or the financial damage may already be done.

When a low-cost divorce may be fine

There is a place for simpler, lower-cost options.

If a marriage has no meaningful assets, no pensions of value, no property, no business interests, no maintenance issue and no dependent children, the risks may be low. In that kind of case, people may reasonably decide that a lighter process is enough.

But that is not the position for many couples.

If there is a family home, a pension, a business, investment property, inheritance, children, financial dependence or a major gap in income, the divorce should be treated with care.

That does not mean it has to be dramatic. It means it should be done properly.

Cheap is not always good value

Everyone wants to keep legal costs under control. That’s sensible. But cost has to be measured against risk.

If there is very little at stake, a cheap divorce may be good value. If there is a home, pension, business or long-term financial security at stake, cheap can become very expensive.

Sometimes the right question isn’t “What is the cheapest way to get divorced?”

It’s “What do I need to understand before I agree to this?”

This is a particularly important question for people with high-value assets.

A divorce is not just the end of a marriage. It is a financial settlement that may shape the next stage of your life.

Before you choose the cheapest route, make sure you understand what it could cost you.

A good family law solicitor should be able to give you a clear view of your position and a roadmap.

Get advice before you agree to anything

If you have a family home, pensions, business interests, inheritance, investments, or other significant assets, it is worth getting proper advice before terms are agreed.

At The Family Practice, we help clients understand what is really at stake, what a fair outcome may look like, and where a quick agreement could cause problems later. The decisions made during divorce in Ireland can shape your finances for years, so it is better to understand your position and speak to a local family law solicitor before signing anything.

Jeremy Ring is a senior family law solicitor and co-founder of The Family Practice in Dublin.

Over his 15-year career, he has advised clients in divorce and separation cases involving combined assets exceeding €10 million, including business valuations, pensions, and inherited property.